Applied AI

How We Built an AI Credit-Scoring Engine That Approves Loans in Seconds

When a borrower applies for a loan, the gap between “application submitted” and “decision returned” is where most lending businesses lose money, customers, or both. Manual underwriting is slow, inconsistent between reviewers, and hard to audit after the fact. Below is how we approach building a real-time credit-scoring engine that returns a decision in seconds, with the explainability and fairness controls that lending actually requires.

The problem with manual underwriting

A human underwriter reading a file is doing something genuinely skilled: weighing income stability against existing obligations, noticing that a recent address change lines up with a job move, judging whether a thin credit file is a red flag or just a young borrower. The problem is not that humans are bad at this. The problem is that they are slow, expensive, and inconsistent. Two underwriters can read the same file and reach different conclusions. The same underwriter can reach different conclusions on a Friday afternoon than on a Monday morning. And none of it scales: doubling loan volume means roughly doubling headcount.

Automating the decision fixes the speed and consistency problems, but it introduces a new obligation. A machine that declines someone has to be able to say why, in terms a regulator and the applicant will both accept. That constraint shapes every engineering decision downstream.

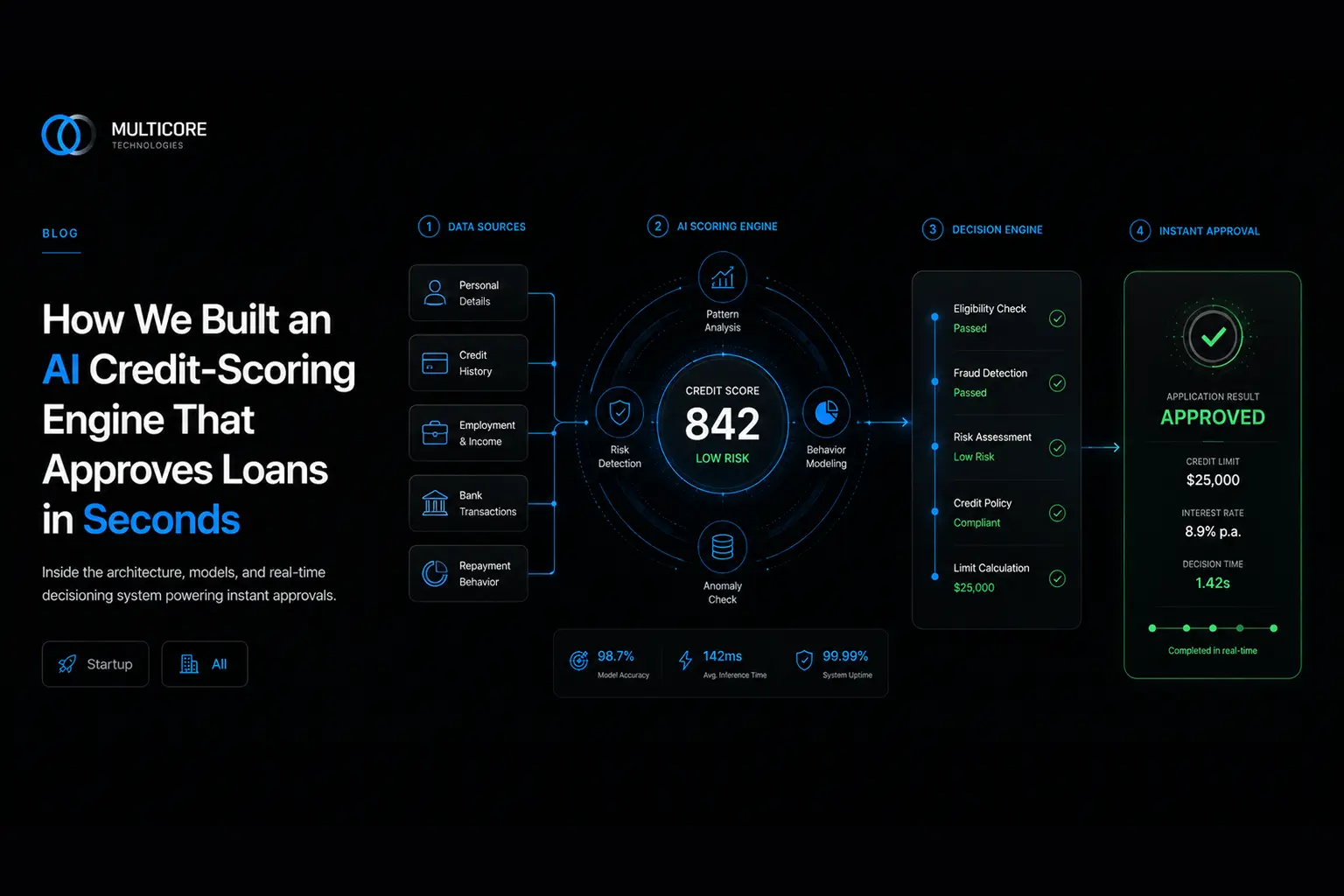

The decision pipeline

A credit decision is not a single model call. It is a pipeline, and most of the engineering effort goes into the stages around the model rather than the model itself.

| Stage | What happens | Why it matters |

|---|---|---|

| Ingest | Pull and normalise data from the application form, credit bureau, and bank-transaction feeds (often via aggregator APIs). Validate, deduplicate, handle missing or stale fields. | Garbage in, garbage out. Most “model” failures are really data failures — a null where a zero was expected, a bureau timeout silently treated as “no record”. |

| Feature engineering | Derive the variables the model actually scores on: debt-to-income, transaction-cashflow volatility, credit-utilisation trends, delinquency recency. Apply the exact same transforms used at training time. | Training/serving skew is the most common silent killer. The feature that meant one thing in the training set must mean exactly that thing in production. |

| Score | Run the engineered feature vector through the scoring model to produce a calibrated risk estimate (for example, a probability of default on a 0–1000 illustrative scale). | This is the fast part. A well-built tabular model scores in single-digit milliseconds. The score is necessary but not sufficient — what surrounds it does the real work. |

| Decide | Apply policy rules and thresholds: auto-approve above a cutoff, auto-decline below another, route the band in between to human review. Layer in hard policy gates (fraud flags, regulatory exclusions). | The model proposes; policy disposes. Thresholds are a business and compliance decision, not a data-science one, and they need to be changeable without retraining. |

| Explain & log | Generate per-decision reason codes (the factors that moved the score most), and write an immutable record of inputs, model version, features, score, and outcome. | This is what makes the decision defensible. Adverse-action reasons, audit trails, and reproducibility are legal requirements in most lending markets, not nice-to-haves. |

Where the data comes from

Three sources carry most of the signal: the application itself (declared income, loan purpose, amount), the credit bureau (history, existing obligations, prior delinquencies), and bank-transaction data (actual cashflow, income verification, spending volatility). Each arrives in a different shape, at a different latency, with a different failure mode. The bureau call might take 800 ms; the aggregator might take longer or return partial data. Designing for graceful degradation — a sensible decision path when one source is slow or unavailable — matters more than any individual feature.

The scoring model: tabular beats LLM here

There is a strong temptation right now to reach for a large language model for everything, including this. For structured credit data, that is the wrong instinct.

Credit decisioning operates on tabular data: rows of numeric and categorical features. For this shape of problem, gradient-boosted decision trees (XGBoost, LightGBM, CatBoost) are not just adequate — they are usually the better choice. They train on your actual portfolio, capture non-linear interactions between features, run inference in milliseconds, and — critically — expose feature attributions through methods like SHAP that map cleanly onto the reason codes regulators expect. They are also small, cheap to serve, and deterministic: the same inputs produce the same output every time, which matters enormously when you have to defend a decision.

A managed LLM or API has a real role in a lending stack, but it is around the edges, not at the core of the credit decision: parsing unstructured documents, summarising a file for a human reviewer, extracting fields from a messy bank statement PDF, drafting an explanation in plain language. What you should not do is let a non-deterministic, hard-to-audit, hallucination-prone model make or directly justify the approve/decline call on structured data. The tabular model decides; the LLM, where used, assists with language and unstructured input. Keep that boundary clean.

Hitting the sub-second budget

“Seconds” is a product promise; “sub-second for the model path” is the engineering target that makes it real. A realistic budget looks like this: external data calls (bureau, aggregator) dominate and run in parallel, not in series; feature engineering and scoring together should sit comfortably under 50 ms; policy evaluation and logging add single-digit milliseconds.

The work that buys you this budget is mostly unglamorous. Fetch external sources concurrently and set hard timeouts with fallbacks. Cache bureau pulls within their validity window so a retry does not mean a second paid call. Precompute and store feature definitions so transformation is a lookup, not a recalculation. Keep the model in memory, not loaded per request. The model itself is rarely the bottleneck — the network calls and the data plumbing are, and that is where the latency engineering actually happens.

Guardrails are the product

In most domains, fairness and explainability are good practice. In lending, they are the job. A credit engine that is fast and accurate but cannot explain itself or treats protected groups inconsistently is not a viable product — it is a regulatory liability.

Three controls are non-negotiable. Explainability: every decision, especially every decline, must produce specific adverse-action reasons — the actual factors that drove the outcome, derived from the model’s own attributions, not a generic template. Fairness testing: the model must be tested for disparate impact across protected classes, before launch and continuously after, because portfolios drift and a model that was fair last quarter may not be this one. Auditability: every decision is logged immutably with its full context — inputs, feature values, model version, score, threshold, outcome — so any decision can be reconstructed and defended months later.

Alongside these sits model documentation: a clear, maintained record of what the model was trained on, what it scores, its known limitations, and its validation results. This is what your risk and compliance teams hand to a regulator, and building it as you go is far cheaper than reconstructing it under audit pressure.

Integration into loan origination

None of this is useful in isolation. The engine plugs into the loan-origination flow as a service: the origination system sends an application payload to a scoring API, the engine orchestrates ingestion, scoring, decisioning, and logging, and returns a structured response — decision, score, reason codes, and a review flag where applicable. Clean API contracts, versioning, and idempotency matter here, because this endpoint sits on the critical path of someone getting or not getting a loan. It has to be boringly reliable.

Building this class of system is less about the model and more about the engineering and governance around it: clean data pipelines, the right model for the data shape, honest latency budgets, and guardrails treated as core features rather than afterthoughts. This is the kind of work we do in our AI engineering work — production systems where correctness, auditability, and fairness are requirements, not aspirations. If you are building real-time decisioning into a lending product, start a project and we will walk through the architecture with you.